Receiving a GST scrutiny notice can be overwhelming for any finance team. However, under the Goods and Services Tax (GST) framework, the department uses a routine, non-intrusive verification mechanism to ensure data consistency.

A scrutiny notice is not always an allegation of tax evasion; instead, it is an investigation into data discrepancies. Understanding the technical nuances of these notices, particularly those issued under Section 61 of the CGST Act, and responding precisely can help businesses avoid penalties, interest, or escalation into full-fledged audits under Section 65.

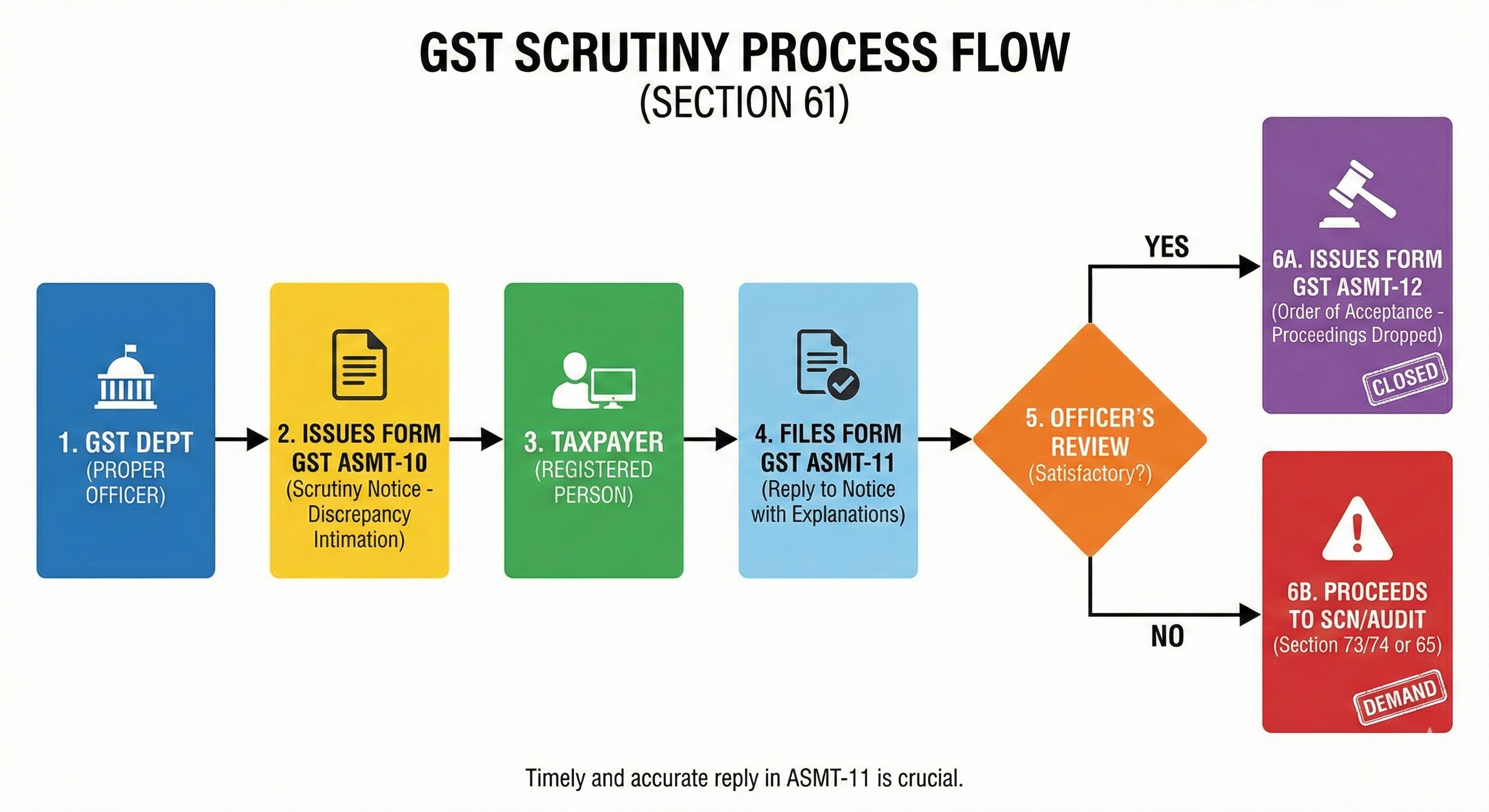

This guide covers the technical grounds for scrutiny, the workflow from Form ASMT-10 to ASMT-12, and how to use automation to effectively manage compliance.

What Is ASMT 10(Scrutiny Notice) In GST?

A GST scrutiny notice is a formal communication issued by the appropriate officer to verify the accuracy of returns filed by a registered person. This procedure is governed by Section 61 read with Rule 99 of the CGST Rules, 2017.

If the officer discovers a discrepancy, such as a mismatch between the declared liability and the tax paid, they will issue Form GST ASMT 10. This notice describes the discrepancies and requires the taxpayer to provide an explanation or pay the differential tax plus interest.

The goal is preliminary verification. If the response is satisfactory, the case is dropped. If not, the case may proceed to a demand notice under Sections 73 (non-fraud cases) and 74 (fraud cases).

Technical Triggers: Why Are Scrutiny Notices Issued?

In the current digital tax administration, the GSTN portal uses Advanced Analytics and Artificial Intelligence to detect inconsistencies. Notices are rarely generated at random; rather, they are triggered by specific data points.

1. Output Tax Mismatch (GSTR-1 vs. GSTR-3B)

The most common trigger is a discrepancy between the liability declared on GSTR-1 (Outward Supplies) and GSTR-3B (Summary Return).

- Technical Example: If you declare a taxable turnover of ₹10 Lakhs in GSTR-1 but pay tax on only ₹8 Lakhs in GSTR-3B, the system flags this short payment immediately.

2. ITC Mismatches (GSTR-3B vs. GSTR-2A/2B)

Excessive Input Tax Credit (ITC) claims are a key focus. If the ITC claimed in Table 4(A)(5) of GSTR-3B is greater than the ITC available in the auto-populated GSTR-2B statement, there is cause for concern.

3. HSN and Rate Classification Errors

Officers review the HSN codes reported to ensure that the correct tax rate is used.

- Technical Example: If a business supplies "Automotive Parts" taxable at 28% but uses an HSN code attracting 18%, this discrepancy in the rate of tax will trigger an inquiry.

4. Ineligible ITC and Blocked Credits

Claiming ITC on goods or services prohibited by Section 17(5) (for example, food and beverages, personal use vehicles) is frequently scrutinized if discovered during data analysis.

5. E-Way Bill vs. GSTR-1 Variance

Significant differences between the turnover projected via active E-Way Bills and the turnover reported in GSTR-1 indicate that sales may be underreported.

How to Reply to a GST Scrutiny Notice (Step-by-Step)

Form ASMT-10 requires a structured, evidence-based approach. The response is submitted using Form GST ASMT-11.

Step 1: Analyze the Notice (ASMT-10)

Look closely at the "Discrepancy Parameter." Is it a tax rate issue, a turnover discrepancy, or an ITC flag? Take note of the fiscal year and the reply deadline (usually 30 days).

Pro Tip: For businesses receiving multiple notices across different GSTINs, manual tracking is risky. Using a GST Notice Extractor can help you instantly capture notice details from the portal and assign them to the relevant team members for action.

Step 2: Perform Data Reconciliation

Before drafting a reply, you must validate the data.

- For Turnover: Reconcile GSTR-1 Table 4 with GSTR-3B Table 3.1 and your Audited Financials.

- For ITC: Reconcile GSTR-3B Table 4 with GSTR-2B and your Purchase Register.

- Technical Example: If the mismatch is due to an invoice reported by a vendor in a later month, identify that specific transaction ID to prove that ITC was validly claimed when it appeared in GSTR-2B.

Step 3: Draft the Reply (Form ASMT-11)

Your reply must be factual and legal.

- If you agree with the discrepancy: Pay the tax, interest (Section 50), and penalty (if applicable) via Form DRC-03.

- If you disagree: Provide a point-wise explanation. Attach reconciliation sheets, sample invoices, and legal precedents if necessary.

Step 4: Submission and Closure (Form ASMT-12)

Submit the reply on the GST Portal. If the officer finds the explanation acceptable, they will issue an order in Form GST ASMT-12, signifying that the scrutiny proceedings are dropped.

The Role of Automation in Handling Scrutiny

Manual reconciliation of scrutiny responses is error-prone, especially when dealing with thousands of line items. Modern tax teams rely on automation to ensure accuracy and speed.

1. Automated Data Extraction

Logging into the portal to check for notices every day is inefficient. An automated system can collect notices, sort them by urgency, and notify stakeholders.

2. Intelligent Reconciliation

To defend ITC claims, you need a robust reconciliation history. Tools that offer Auto ITC Reconciliation allow you to match your purchase register with GSTR-2B in real-time, identifying missing

invoices or vendor errors before the department flags them.

3. Vendor Compliance Management

Many notices stem from non-compliant vendors who fail to file returns. Using a Verify GSTIN Tool during vendor onboarding ensures you only deal with compliant suppliers, significantly reducing downstream mismatches.

Consequences of Ignoring a Scrutiny Notice

Failure to reply to Form ASMT-10 or providing an unsatisfactory explanation has serious legal implications:

- Demand Order: The officer may initiate proceedings under Section 73 or 74, issuing a Show Cause Notice (SCN) in Form DRC-01.

- Audit: Persistent discrepancies may trigger a departmental audit under Section 65.

- Interest & Penalties: Interest under Section 50 accumulates daily. Delayed action increases the financial burden significantly.

Final Thoughts: Moving from Reactive to Proactive

GST scrutiny notices are a necessary part of the compliance process. The key to managing them is not only a good response, but also a proactive data strategy. Businesses that maintain "audit-ready" data through continuous reconciliation and automated notice management are far better positioned to deal with scrutiny confidentially.

Using spreadsheets to manage large GST datasets is a liability. Adopting an AI-enabled compliance system guarantees that when the department asks a question, you will have an immediate, accurate response.

Sepfust Solutions provides tax and finance automation for SAP & Oracle ERPs. Their "Smart Cockpit" add-ons—including Auto-ITC Reconciliation, GST Notice Extractor, and E-Invoicing—integrate directly with government APIs, eliminating manual errors and external portal dependency for seamless compliance.

Kunal Jaitly

Kunal Jaitly is a seasoned Tax-Technology leader with over 20+ years of experience spanning Taxation, Finance, and ERP-driven automation. With a strong Big 4 consulting background, Kunal has led and delivered large-scale tax and compliance transformation programs for enterprises across industries.

As the Founder of SEPFUST, he brings deep domain expertise and a practitioner’s mindset to building SAP-native and cloud-based automation solutions that simplify compliance, enhance accuracy, and unlock the true potential of enterprise systems. His work bridges the gap between complex tax regulations and scalable technology, enabling organizations to move from manual processes to intelligent automation.